Strong non-farm payrolls numbers proved irrelevant as a short-lived dollar rally was quickly dismissed by investors. The equity rally continue to prove disappointing for investors expressing their risk-on trade through euro and yen as the dollar loses steam while risk sentiment recedes. USDSGD also touched two-month lows on the back of dollar weakness, quarter-end FDI profits repatriation and repricing of risk from EM Asia as oil edges higher. As we begin a month of central banks’ meetings, namely the ECB (10/3), BOJ (15/3) and Fed (16/3), it may provide another opportunity for central bankers to convince financial markets of its ability to boost inflation.

In this piece, I provide a preview of ECB possible policy actions. Wounds are still raw when Mario Draghi underwhelmed markets at the December policy meeting. Yesterday, the euro snapped higher on rumours that the governing council (GC) is lacking consensus going into the policy meeting. While rates market has been pricing in a rate cut next week, EURUSD seems unfazed and stood at 1.10 at time of writing.

Recent economic activity

Recent data broadly painted a bearish outlook for the Eurozone. Composite PMI declined 0.9 to 52.7, while German Ifo took a dive to 105.7 from 107.3. Industrial production from the three biggest Eurozone economies, Germany, France and Italy, all declined in December. Most importantly, February consumer prices fell into negative territory of 0.2%, lowest since March 2015. Core inflation (excl. energy, food, alcohol and tobacco), on the other hand, declined to 0.7% yoy from 1.0%. Yet, the euro appreciated by 1.4% since January policy meeting.

Continued divergence reflected in Citi’s Economic Surprise Index for U.S. and Europe (Source: Thomson Reuters)

What’s priced in?

While it is difficult to analyse what exactly is priced in into the market given the diverse policy tools available, most sell-side reports suggest markets has priced in around 10bp cut. This is reflected from the European rates market while investors remain cautious of EURUSD as wounds are still raw from December disappointment.

Will Draghi deliver this time?

Back in January, Draghi said the Governing Council will “review and possibly reconsider our monetary policy stance at our next meeting.” While Draghi is known for jawboning the euro with his choice of words, the market was not expecting such explicit form of guidance. All banks on the street expect ECB to do more in the next meeting.

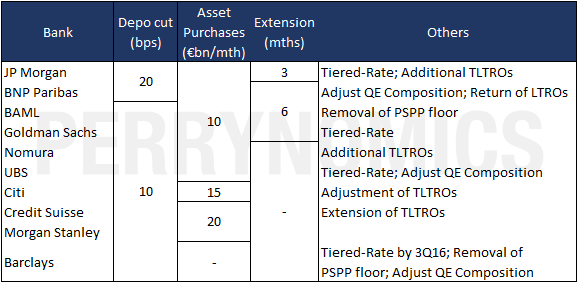

Wall Street Expectations: All banks expect the ECB to expand QE programme

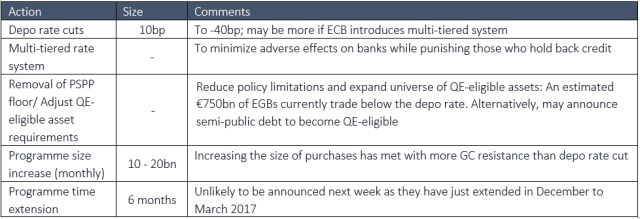

Possible Policy Options: I expect a depo rate cut of 10bps and an increase of monthly asset purchases by 10-20bn. If a multi-tiered rate structure is introduced, the size of depo rate cut could be bigger.

Given the recent turmoil in the European banking sector and comments by some governing council members about the negative impact of negative interest rates, I continue to expect that ECB will introduce a multi-tier rate system at some point.

The following week will be relatively quiet on US economic data. Therefore, the deciding factor of the EURUSD direction will largely be dependent on Draghi’s decision. (Of course, risk sentiment may turn sour if markets decide to think central banks have lost their effectiveness to support asset prices. This is not my base case.) It is critical that Draghi sends a credible commitment to support inflation expectations and convince investors that the GC is not out of ammunition.

Best,

P