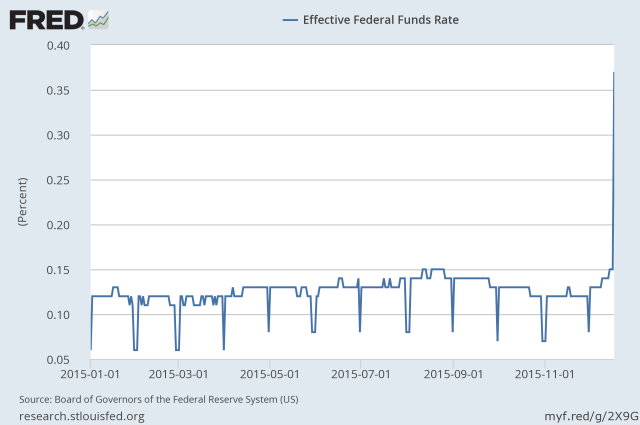

A question popped up on my mind as to why there is a plunge in Effective Fed Funds rate and also why it broke the RRP floor on Dec 2015.

Short answer

Month-end Plunge: GSEs (notably FHLBs like Fannie Mae) do not have access to IOERs and earn zero interest on their cash. Hence, they lend it out in the Fed Funds market to earn interest. Near month-end, banks face higher balance sheet usage as borrowings cause stress on their leverage ratio. Hence, they need to be enticed to borrow at a lower rate. This explains why we see a plunge near month-end.

RRP Floor: On why the floor broke on 31 Dec 2015, it is worth noting that it has only broken once since RRP’s inception, on the last day of the year with thin liquidity. I won’t read too much into it. Theoretically the floor should always hold since GSEs have access to ON RRP, unlike IOER.

Background information

Dynamics of GSEs and banks in the Fed Funds market: GSEs, having no access to IOER, often lend their reserve balances overnight on the fed funds market to commercial banks. These commercial banks could then hold the funds as reserves overnight, earning 0.25%, while paying the GSEs x%, where 0 x 0.25, to make a profit (Under PC market, x = 0.25, since there are limited number of GSEs). Indeed, ~75% of lending on the fed funds market was accounted for by FHLBs (2012).

However, financial institutions that receive IOER also face balance sheet costs associated with borrowing on the fed funds market. This includes FDIC cost, which since Dodd Frank has become dependent on total balance sheet assets as well (only for US banks). This gives foreign banks a cost advantage, which means they will be the main agent to borrow from FHLBs to arbitrage the IOER-FFR spread. This explains why ~60% of borrowing on the fed funds market was being done by foreign-owned banks.

Best,

P

Disclaimer: Perry is a summer analyst at JP Morgan. This is his personal view.